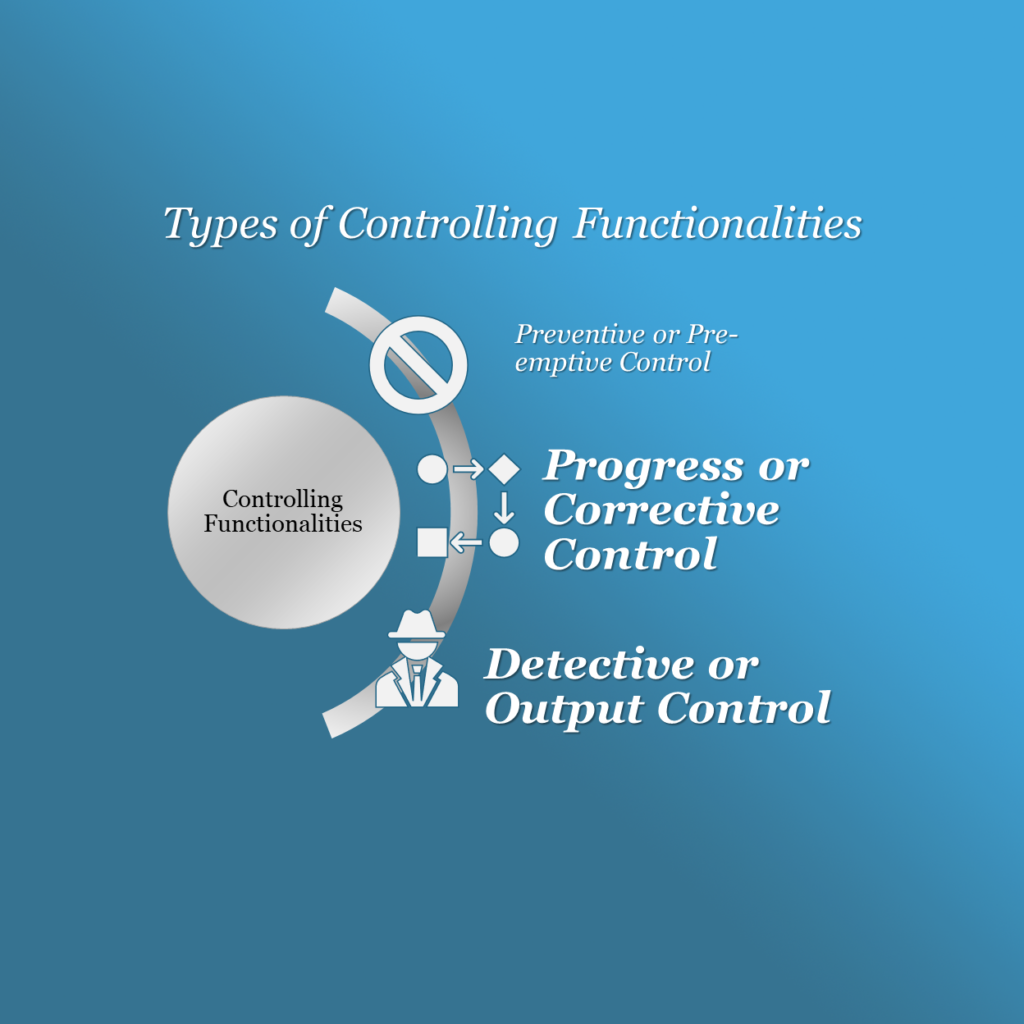

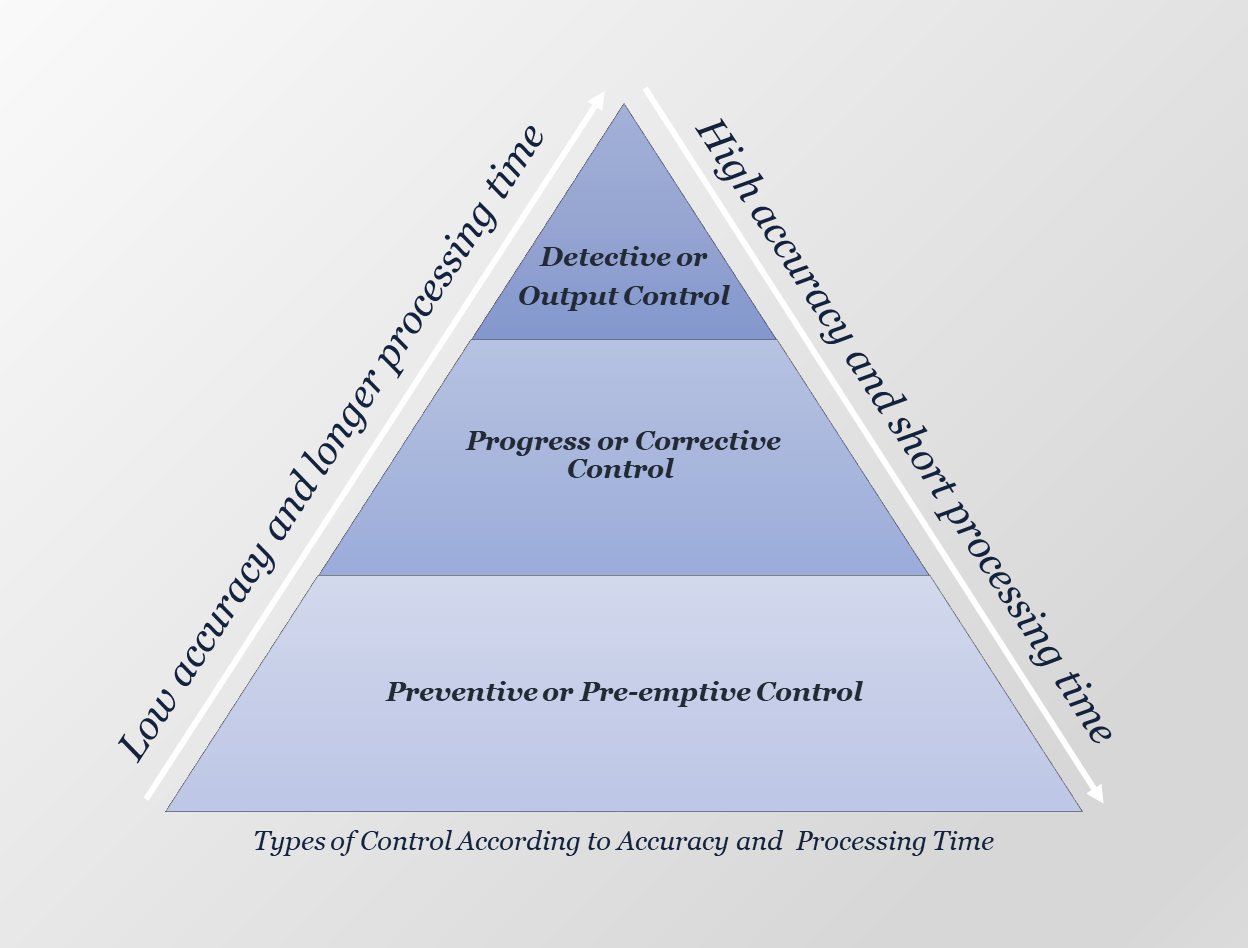

2nd & 3rd Controlling Types - Progress Control and Detective Control

Progress Control and Detective Control

Since we have discussed in a previous article; the controlling types in terms of time: (Preventive Control – Progress Control- Detective Control), and the concept of the first type “Preventive Control” in another article, here we are going to discuss The other types.

In our article, we are going to clarify the two concepts of Progress Control and Detective Control, and compare the two types in terms of time, techniques, stages, and advantages. So that, you can understand how each control can figure out the weaknesses that may hinder the operations, projects’ implementation, or post-implementation.

It should be noted that managers and companies should understand what controlling is, and know how it must function professionally in order to achieve businesses’ objectives and goals.

Progress Control

Progress control follows up on the projects’ implementation in order to detect schedule, resource, budget deviations, and faults immediately, then make the appropriate corrective actions. Progress control doesn’t use prediction, as in preventive control, which makes it easy-going progress requiring no administrative skills of prediction, forecasts, or intuition.

Detective Control

Detective Control is designed to find errors or irregularities after they have occurred. It provides valuable options for amending and correcting the subsequent processes. It won’t change what has taken a place during the implementation progress, but it can avoid future faults for it is based on the final outcomes. There is much time in this type to make the right decisions because it begins when operations end.

Progress & Detective Control Tools

There are 5 types of control tools:

- Financial Tools: financial budgets, cyclical budgets of a (project/company), income statement, achievement percentage and financial efficiency of the company, and financial ratios

- Productive Tools: inventory, efficiency, productivity

- Quality Tools: Pareto chart, Statistical Quality Control (SQC)

- Earned Value management: critical inputs, proportionality rule

- Critical ratio: It uses the Schedule performance index (SPI) and cost performance index (CPI)

Preventive Control relies upon the information and readings of the former learned lessons in the company, plus the inputs of the projects.

Progress Control uses plans, proposals, and schedules of (time, cost, time…etc.), budgets, financial and productive phased outcomes, and tools of (quality, earned value, and critical ratios.)

Whereas, Detective Control depends on the company’s objectives, financial budgets, learned lessons, and final reports.

It is worth noting that the control system can choose the appropriate tools in order to deliver the best outputs; Pareto chart or earned value … etc., which would distinguish between companies in terms of controlling system’s efficiency.

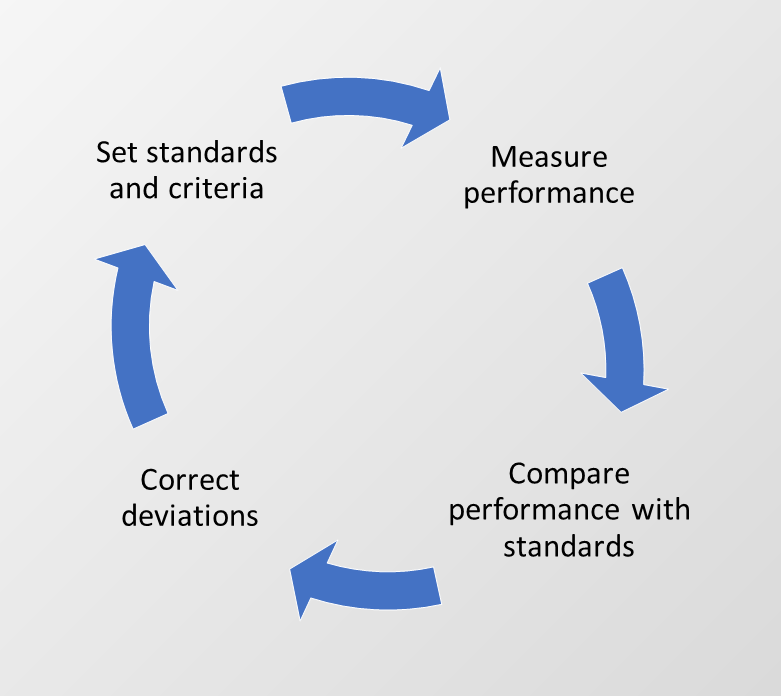

Stages of Progress Control and Detective Control

Whatever the type of control is, it goes through the same stages:

- Set standards and criteria

- Measure performance

- Compare actual performance with pre-determined standards contained in the plans.

- Correct deviations

The controlling process output is learned lessons. It may lead to major changes; such as Reengineering the company’s operations, or re-examining the objectives and strategies (such as; the techniques of correcting deviations, rectifying faults, and solving problems, … etc.)

Controlling systems through all stages should be compatible with the business’ volume and environment, and must be certain that no matter what the problems or obstacles that hinder the business progress are, there are always efficient solutions.

Preventive controls are crucial for maintaining the integrity of an organization’s operations, financial reporting, and compliance with laws and regulations. By preventing issues before they occur, organizations can avoid costly mistakes, reduce the risk of fraud or errors, and maintain their reputation with stakeholders.